Week 3-2 of the AWS MLops: AWS Forecast and time-series data

Forecasting and AWS Forecast#

Overview#

- Predicting future values that are based on historical data

- Patterns include

- Trends

- Seasonal, pattern that is based on seasons

- Cyclical, other repeating patterns

- Irregular, patterns that might appear to be random

- Examples

- Sales and demand forecast

- Energy consumption

- Inventory projections

- Weather forecast

Processing time series data#

Time series data is captured in sequence over time

Handle missing data

- Forward fill

- Backward fill

- Moving average

- Interpolation: linear, spline, or polynomial

- Sometimes zero is a good fill value

Reasmpling: Resampling time series data allows the flexibility of defining resolution of the data

- Upsampling: increase the sample frequency, e.g. from minutes to seconds. Care must be taken in deciding how the fine-grained samples are computed.

- Downsampling: decrease the sample frequency, e.g. from days to months. Need to pay attention to how the aggregation is carried out.

- Reasons for resampling:

- Inspect the behavior of data under different resolutions

- Join tables with different resolutions

Sampling smoothing, including outlier removal

- Why

- Part of the data preparation process

- For visualization

- How does smoothing affect the outcome

- Cleaner data to model

- Model compatibility

- Production improvement?

- Why

Seasonality

- Hourly, daily, quarterly, yearly

- Spring, summer, fall, winter

- Holidays

Time series sample correlations

- Stationary

- How stable is the system

- Does the past inform the future

- Trends

- Correlation issues

- Autocorrelation

- How points in time series sample are linearly related

- Stationary

pandasoffer many methods for handling time series data- Time-aware index

groupbyandresample()autocorr()method

Times series algorithms offered by Amazon Forecast

- ARIMA, autoregressive integrated moving average

- DeepAR+

- Exponential Smoothing (ETS)

- Non-Parametric Time Series (NPTS)

- Prophet

Model evaluation

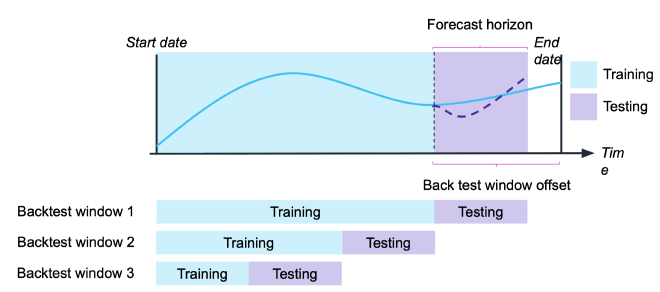

- Time series data model training cannot use $k$-fold cross validation because the data is ordered and correlated.

- Standard approach: back testing

</figure>- Two metrics can be used to access the backtesting (hindcasting instead of forecasting) accuracy

- wQuantileLoss: the average error for each quantile in a set

- RMSE, root mean square error